Indian economy – the greatest show on earth

Dear Patron,

The world is glued to the 2022 FIFA world cup, the greatest show on Earth, which kicked off in Qatar. With Asian and African teams taming footballing giants, the world cup has been a tournament of "upsets". It is difficult not to draw parallels between the upsets in the world cup and that of the world economy. With China's economy slowing, India is catching up and potentially on track to become the world's third-largest economy sooner than previously expected. In the face of global recessionary concerns, the Indian economy is the "breakout star" of an otherwise anaemic global economy.

As the Indian economy continues to show resilience, Nifty50 has surpassed its previous all-time high. Experts believe the rally in the Indian stock market is going to stay for a while now with short-term volatility due to global factors. In the last month, the Nifty has rallied ~5%, while the mid and small-cap indices are up by <2% each. The second quarter results have displayed the strength of the Indian economy amid fears of a global recession.

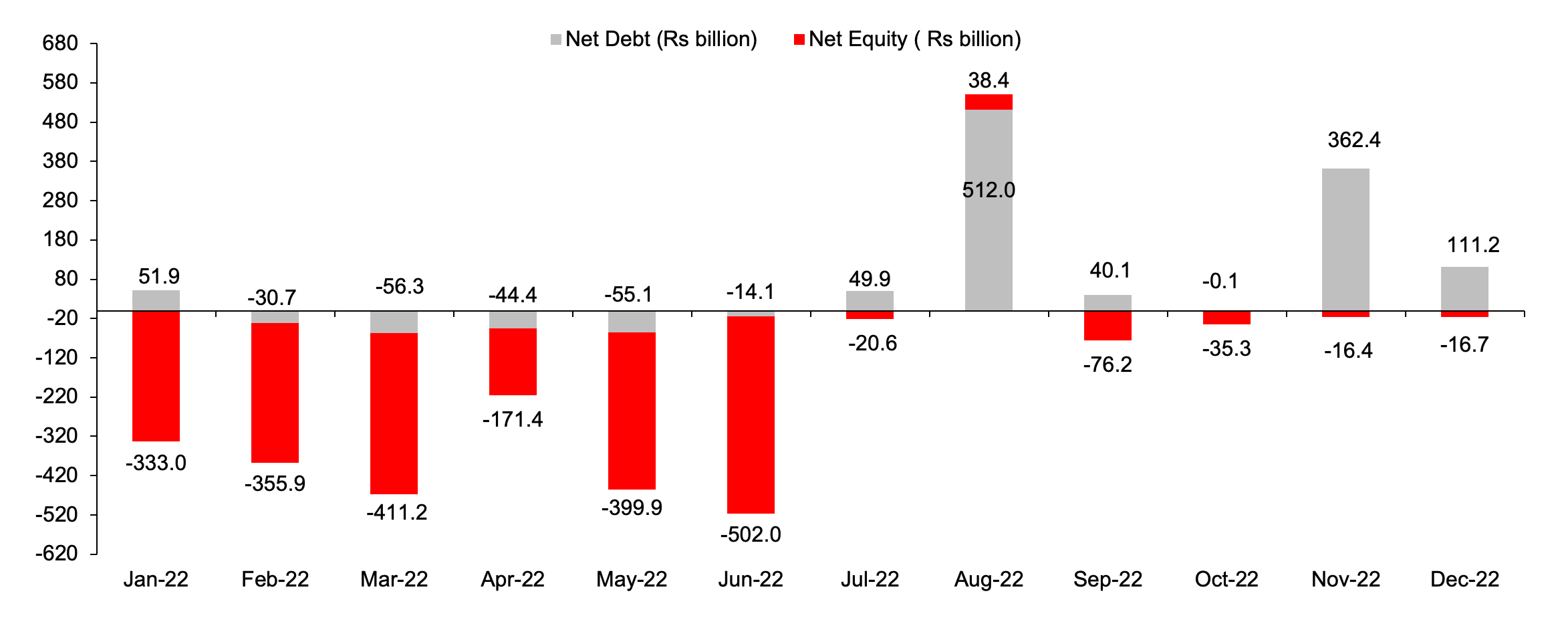

Exhibit 1: Increased FPI inflow (in $billion) as the US Federal Reserve officials expect to switch to lower pace of interest rate increase

Source: NSDL, ET Money, Ambit Asset Management

Q2FY23 Portfolio Revenue/EBITDA/PAT snapshot

Exhibit 2: Superior profitability across our portfolios in a challenging quarter

Source: Company, Ambit Asset Management

Performance of different sectors for the Q2FY23 quarter

Consumer - Staples

Subdued rural demand leads to weak volumes – Revenue recovery on a lower base stemmed from nil disruption to operations and strong festive demand which aided double-digit revenue growth for the FMCG companies. Volume growth of the sector was muted led by macro challenges particularly in rural segment, with managements highlighting that rural growth lagged urban growth for the first time in the past few years. The 3yr value growth, for most companies, is at double digits aided by material price increases taken across categories.

Exhibit 3: Staples witnessed muted volume growth whereas retail segment (GT) saw down‐trading to LUPs/small pack

Source: Company, Ambit Asset Management

Inflation rate likely peaked – Prices of daily consumables like cereals and vegetables have climbed over the past two years due to erratic rainfall and supply shocks from Russia's invasion of Ukraine. The sustained high prices of certain raw materials especially agri-related and high cost inventories have led to continued margin pressure.

Exhibit 4: Retail Inflation staying above the Reserve Bank of India's (RBI) upper tolerance band for a ninth month.

Source: RBI, Ambit Asset Management

Consumer - Discretionary

Key Trends in Discretionary segment: Contrasting demand trends were witnessed owing to the divergent impact of inflation on the rural vs. urban discretionary spends. K shaped recovery was witnessed with Tier-1/2 cities continued to outperform Tier3 and below cities with increasing share of premium range (Premiumization) while Mass/value segments remained under pressure due to high inflation. Robust footprint expansion and deeper penetration into Tier 2/3 cities witnessed across the retail pack to capture additional market share.

Resilience in profitability despite a mixed bag on inflation: Operating profitability remained resilient, despite a mixed bag on the inflationary situation, aided by operating leverage benefits and Premiumization efforts. While the prices of key RM witnessed some softening during 2QFY23, the high-Cost inventory carried by companies had an impact on profitability particularly in footwear industry. Ecommerce/ digital channels growth momentum sustained in 2QFY23 for most categories & increased up to ~20% for companies across the discretionary pack.

Auto & Auto Ancillaries

Volume recovery getting broad based – Domestic auto volumes in 2QFY23 recovered across segments, supported by improvement in the supply of semiconductor chips and early festive season demand. Wholesale numbers for passenger vehicles were up 40% YoY, 2Ws up 28% (scooters +40% YoY) have outperformed motorcycles (+24%) in H1), 3Ws up 106% and CVs were up 68% YoY in H1FY23. On the Export front, the second quarter saw moderation in exports. This was due to inventory destocking, in anticipation of weak demand, on-going geopolitical conflicts and the depreciation of the currency.

Exhibit 5: Wholesale volumes high led by festive as well as structural demand push

Source: SIAM, Ambit Asset Management

More EV’s on the anvil –India saw 5x/3.6x growth in EV2w/ Electric cars in H1FY23 Companies are planning to launch more EV models. TVS iQube (now in 33 cities) will soon be available around the country by year end. Bajaj Auto plans to increase its reach in 20 cities by FY22-end and to install a capacity of 0.5mn units for E-2Ws. M&M plans to launch EVs in SUV, LCV, 3W and tractor segments over the next 4-5 years while Ashok Leyland is launching an electric LCV.

Financials

Growth – Credit growth inched up from low double digit to high mid-teens (broad-based) which translated into higher Net Interest Income growth along with margin expansion. Deposit growth still lags the credit growth. Housing finance companies continue showing healthy signs on AUM & disbursement growth but operating growth lags balance sheet growth on account of lead-lag effect. Operating profit lags revenue growth due to higher operating expenses but lower credit cost on account of benign asset quality led to superlative profit growth driving the overall index growth.

Exhibit 6: Broad based Credit growth witnessed during the quarter (in %)

Source: RBI, Ambit Asset Management

Exhibit 7: Strong growth in loan disbursements across segments (in %)

Source: RBI, Ambit Asset Management

Margins - Loans have been reprised on account of rise in external benchmarks i.e. Repo rate. Overall NIMs have risen YoY & QoQ for banks whereas few NBFCs have a higher portion of book on fixed side resulting in NIM pressure due to lead-lag effect.

Asset Quality - Balance Sheet strengthen through higher PCR as well as recoveries which were at par or higher than slippages. GNPA & NNPA trends have been at 28 quarters low for both PSU & Pvt sector banks. Asset Quality for HFCs & NBFCs improved sequentially but remains sub-par compared

Exhibit 8: GNPA for private and PSU banks at 28 quarter low (in %)

Source: RBI, Ambit Asset Management

Exhibit 9: WALR* for outstanding loans inching up in line with Repo rate hike (in %)

Source: Company, Ambit Asset Management. * WALR–Weighted Average Lending Rate

Pharmaceuticals / Healthcare

Diverging growth trends in 2Q23: US business of leading companies witnessed strong growth led by gRevlimid launch, negating the impact of base business price erosion. Custom Synthesis business of most companies (ex Laurus, Syngene) witnessed pressure owing to the innate lumpiness of that segment, with long term growth trends intact. India business (ex-COVID) continued to post stable growth

Margin headwinds easing: Sharp RM price inflation witnessed over the last few quarters is easing, with even decline in some input prices. Freight costs have not yet cooled off but availability has improved leading to further possibility of margin improvement (Refer Exhibit: 11).

Exhibit 10: Cost pressure for top companies abating – which was visible in Q2FY23 margins

Source: Company, Ambit Asset Management

Building Material

Demand scenario and commentary was weak signalling a probable slowdown: Demand slowdown was seen in the larger basket of building materials – particularly in ceramics, paints and adhesives – led by sharp price hikes and rural slowdown. Further, our channel checks suggest that the demand scenario has remained tepid even during the festive season suggesting growth moderation.

Have seen margin pressure in the quarter, larger companies with established brands such as Kajaria have been impacted lower vis-à-vis competition. With easing prices of raw material and gas prices, there is likely to be improvement in margins across most building material sectors going forward.

Exhibit 11: EBITDA margin for ceramic companies have been severely hit due to high energy costs

Source: Company, Ambit Asset Management

Incremental Demand outlook for several pockets in the space such as sanitary-ware, faucet-ware and plastic pipes remains robust owing to benign raw material prices.

Chemicals

The chemical industry posted a big contrast in operating performance with Agriculture - chemical players reporting healthy numbers however other pockets faced several headwinds primarily companies catering to end user segments in pharmaceuticals, textiles and pigments.

Agriculture - chemical companies continued to scale up well both on domestic front led by a decent monsoon and exports front with PI Industries leading the line.

Demand tailwinds remained robust with most chemical companies in the capacity expansion or utilization of expanded capacity. Cool-off in several raw material prices will also provide an impetus to margin improvement going forward.

Information Technology

Cross Currency headwind the only spoil-sport: Severe cross currency impact dragged median USD growth of Tier1/2 companies by ~200/250bps, courtesy sharp decline in Euro and GBP. Understandably, companies with higher exposure to Euro/UK witnessed a sharper impact. Ex of currency there were not many tangible signs of slowdown in growth number barring pockets of weakness such as Rate sensitive Mortgage BPO, Capital Markets, etc. Tier-2 growth outperformance over Tier-1 continued, albeit at a slower pace – an indication of slower discretionary spend.

Margin Recovery in sight: Almost all Tier-1/2 companies witnessed QoQ Margin improvement, barring those that had wage hike impact, which too was lower than anticipated. This corroborates with our view that margin have bottomed out and will only recover from hereon led by (1) Lower Attrition (2) Better Utilization (3) Limited wage hike

Key Trends / Management highlight: (1) Expect normal furloughs going into H2, unlike last year where growth was strong (2) Macro events will not be broad based but more micro based – depending on industry, service offering and geography (3) Signs of attrition cooling off which should further aid margin (4) Lower headcount addition as large pool of fresher hired in T12M will come on board (5) No large deal cancellations but decision cycles are getting elongated.

Exhibit 12: Intensity of attrition has now started to cool off which should further aid margins

|

Attrition chg QoQ (in bps) |

Q2FY22 |

Q3FY22 |

Q4FY22 |

Q1FY23 |

Q2FY23 |

|

TCS |

330 |

340 |

210 |

230 |

180 |

|

Infosys |

620 |

540 |

220 |

70 |

(130) |

|

Wipro |

500 |

220 |

110 |

(50) |

(30) |

|

HCL Tech |

390 |

410 |

210 |

190 |

- |

|

TechM |

380 |

300 |

- |

(200) |

(240) |

|

LTI |

440 |

290 |

150 |

(20) |

50 |

|

Mindtree |

400 |

420 |

190 |

70 |

(40) |

|

Coforge |

270 |

100 |

140 |

30 |

(160) |

|

Persistent |

700 |

330 |

(30) |

(180) |

(110) |

|

LTTS |

200 |

100 |

290 |

280 |

90 |

|

Mastek |

460 |

380 |

- |

(298) |

(82) |

Source: Company, Ambit Asset Management

CONCLUSION:

CY22 was a year marred by headwinds. Despite this, Corporate India – especially our portfolio companies – have weathered the storm well. Heading into the next year, we anticipate these headwinds to dissipate given (1) Cooling of inflation globally (2) Normalized supply chain (3) Easing of interest rate hikes by the central banks. The resilience shown by Indian Economy and Corporate India has stood out globally; with visible signs of ‘+1’ benefits. Investors and corporates alike are now flocking to India which will bode well for long term fundamentals and capital flows. The India story for investors is just getting started!

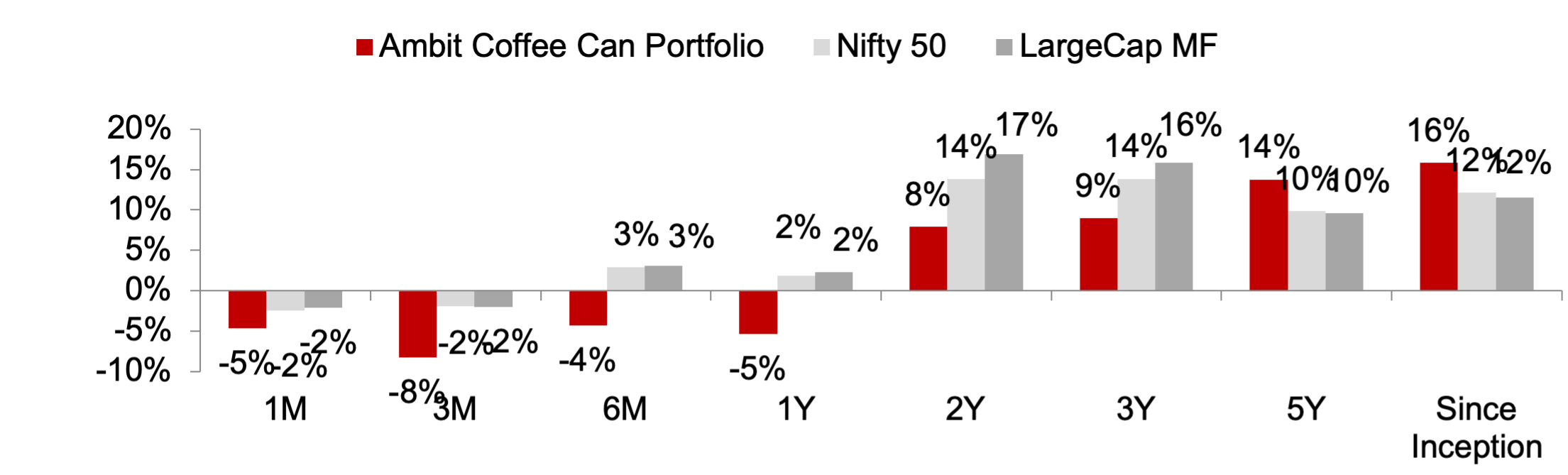

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced by disruptions at regular intervals. As the industry evolves or is faced by disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 13: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of November 30, 2022; All returns are post fees and expenses; Returns above 1-year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Exhibit 14: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of November 30, 2022; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

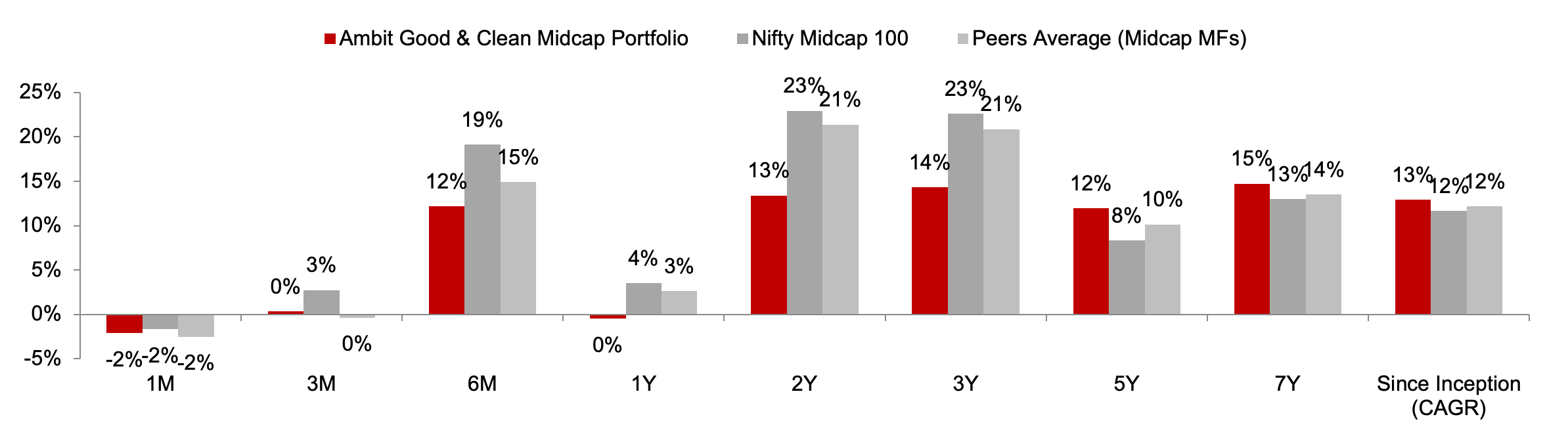

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with this compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 15: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of November 30, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 16: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of November 30, 2022. Returns are net of all fees and expenses

Ambit Emerging Giants Portfolio

Small caps with secular growth, superior return ratios and no leverage –Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt) and ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 17: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of November 30, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 18: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of November 30, 2022. Returns are net of all fees and expenses

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 19: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of November 30, 2022; Returns are net of all fees and expenses

Exhibit 21: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of November 30, 2022. Returns are net of all fees and expenses

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected]

Ambit Investment Advisors Private Limited -

Ambit House, 449, Senapati Bapat Marg,

Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020.